Weekly Coal Index Report

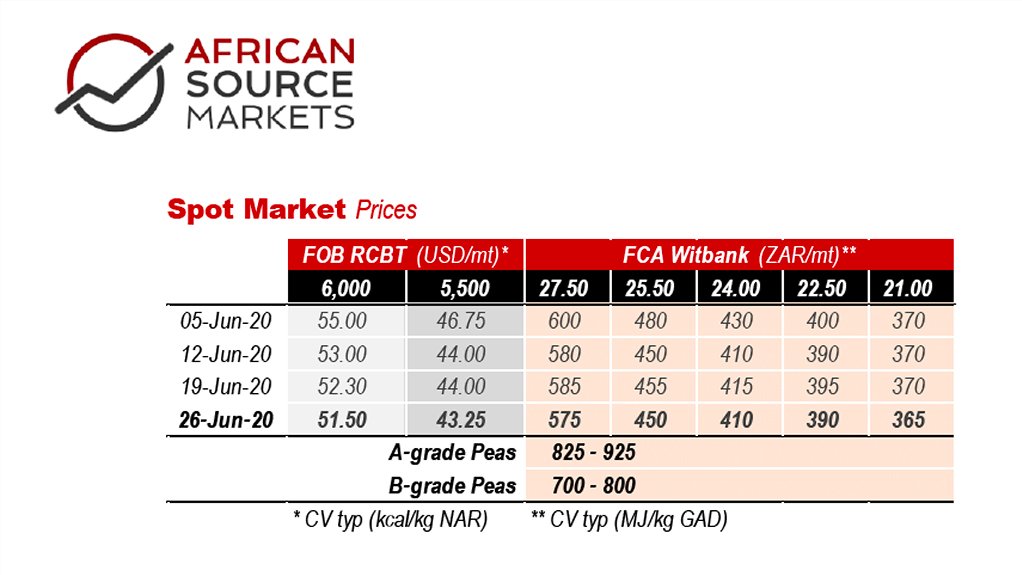

Physical RB1 had another tough week, with at least one cargo going through at around $48/mt. Although Chinese utilities are restocking, they are having to use domestic coal as they lack import quotas from government. This is a trend that the Chinese government wants to see strengthening as it has spent significant cash building out the logistics infrastructure to supply coastal utilities.

Filling the hole left by Chinese demand destruction is an almost impossible task, and will affect mainly Indonesian and Australian suppliers, who will now increasingly target RB1 export markets. Meanwhile, Indonesia’s Coal Mining Association is asking mines to cut their output to prevent further falls in price, caused mainly by lack of demand from China and India. It remains to be seen whether this will be achieved.

At least miners in South Africa can still supply Eskom on both a cost-plus and fixed price basis. However, Eskom CEO Andre de Ruyter said last week that there are several fixed price coal contracts of concern, with six expiring in the next few months.

It is a great time to be renegotiating price, although producers may look to hold back supply for now. Or perhaps exports could even be saved by a weaker ZAR, which could still easily reach 20 to the USD by year end based on current vol.

Comments

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Rooted in the hearts of South Africans, combining technology and a quest for perfection to bring you a battery of peerless standing. Willard...

VISIT SHOWROOM

Rentech provides renewable energy products and services to the local and selected African markets. Supplying inverters, lithium and lead-acid...

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation